")

General liability insurance plays an essential role in keeping businesses financially protected if accidents involving clients and other third parties threaten to derail their operations. That’s why it’s always advisable for companies to take out this form of coverage regardless of their size and the industry they’re in. But how much does general liability insurance cost?

In this article, Insurance Business crunches the numbers to find out how much premiums cost for this type of policy. We will also delve deeper into the factors that affect pricing and explain how rates are calculated.

If you’re working out how much coverage your business needs and how much this will cost you, then you’ve come to the right place. Read on and find out everything you need to know about general liability insurance costs in this guide.

The average cost of general liability insurance for small businesses ranges from $40 to $55 monthly or $480 to $660 per year based on the various price comparison and insurer websites Insurance Business has checked out.

Since the risks that companies face vary greatly depending on a range of factors, their premiums can also be significantly higher or lower than these figures.

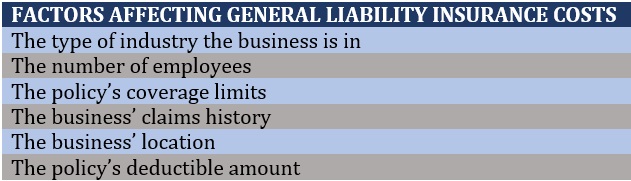

While the estimated average cost of general liability insurance our research found may not seem that high at first glance, it’s important to note that the actual premiums a business will need to pay may go well above or below that amount, depending on the following factors:

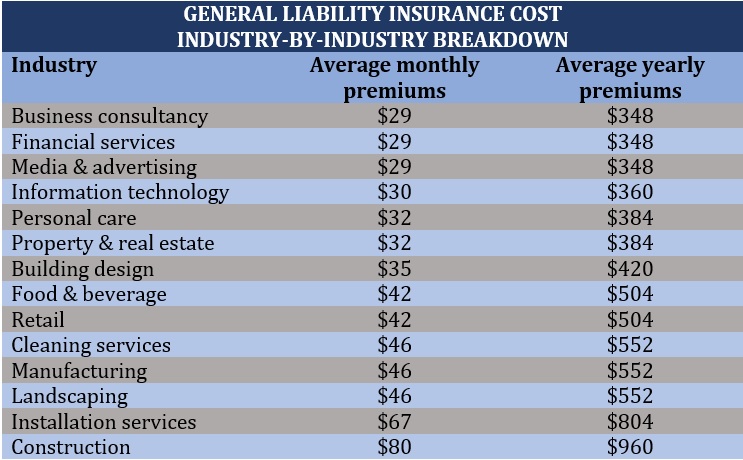

1. Industry

Different industries present varying levels of risks which have a corresponding impact on general liability insurance costs. For example, office-based businesses that don’t experience a lot of foot traffic such as financial and IT consultancies pay lower premiums compared to retailers – which customers frequent and face a greater likelihood of injuries.

Another example is construction and landscaping services which pose a higher risk of property damage.

The table below lists the estimated monthly and annual premiums for general liability coverage for businesses in different industries.

2. Business size

The more employees a business has, the higher the cost of general liability insurance. From an insurance perspective, each staff member carries a certain level of risk. A taxi fleet with 20 or more drivers, for instance, has a higher likelihood of getting involved in an accident compared to a transport service company with five drivers.

3. Coverage limits

When it comes to policy limits, there are two figures that have a huge impact on general liability insurance costs. These are:

-

- Per-occurrence limit: The maximum amount an insurer will pay out for a single claim

-

- Aggregate limit: The maximum amount an insurer will pay out in a year

Per-occurrence limits are typically pegged at $1 million, while aggregate limits are usually set at $2 million. These figures can be adjusted depending on the needs of the business. The higher the limits, the higher the premiums and vice versa.

4. Claims history

Each claim can raise general liability insurance costs come renewal time. Insurance companies view businesses that have faced lawsuits and filed claims to cover their losses as risky and will tend to charge them higher premiums to offset potential future losses.

5. Business location

Businesses based in areas with higher crime and accident rates are more likely to have costlier premiums than their counterparts in safer locations.

6. Deductible amount

The deductible is the amount that businesses must pay out for an insured loss before coverage kicks in. Generally, the higher the deductible, the lower the premiums as the insurer assumes less risks. If you want to find out how this insurance component works, you can check out our comprehensive guide to insurance deductibles.

Here’s a summary of the different factors that affect general liability insurance costs.

Insurance companies typically determine how much premiums a business must pay using a rating system developed by different organizations, including:

-

- Insurance Services Office (ISO)

-

- National Council on Compensation Insurance (NCCI)

-

- North American Industry Classification System (NAICS)

-

- Standard Industrial Classification (SIC)

There are also some insurers that follow their own classification systems. What these rating systems have in common is the use of class codes to determine how much risk a line of business presents.

Apart from this, these codes – which consist of three to six digits depending on the ratings agency – enable insurers to identify what types of coverage a business needs or doesn’t need, so they can come up with an appropriate pricing for the policy.

Although general liability insurance policies are not that expensive, there are still ways for you to slash your premiums. These include:

-

- Purchasing a business owner’s policy (BOP): This type of coverage bundles together several policies, including commercial property, business interruption, and general liability insurance, allowing you to save costs than if you take out separate policies. BOPs, however, are available only to small businesses with fewer than 100 staff and less than $1 million in revenue.

-

- Opt for annual payments: Paying general liability insurance as one lump sum rather than by monthly instalments can result in savings. Doing this helps your business avoid being charged interest or finance arrangement fees.

-

- Manage your business’ risks: Having a spotless claims history is among the best ways of keeping your general liability insurance cost low. These can be as simple as keeping the floor of your establishment dry to prevent people from slipping to implementing a comprehensive safety training program for your employees.

-

- Pay attention to intellectual property rights: Your business can be sued for unauthorized use of images, music, and other intellectual property. To prevent this, make sure that you’re not committing copyright infringement, especially when creating marketing or advertising materials for your business.

General liability insurance – also referred to as business liability or public liability insurance – protects your business financially against claims of bodily injury or property damage resulting from your business activities.

Most policies also include product liability coverage, which covers lawsuits from customers claiming losses or injury because of a product you manufacture or sell.

General liability policies may likewise provide coverage for copyright infringement and incidents that cause reputational harm, including:

-

- Libel

-

- Slander

-

- False arrest

-

- Malicious prosecution

-

- Wrongful eviction

-

- Invasion of privacy

If your business has been accused of causing these types of harm, general liability insurance will cover the legal and settlement costs involved. Such policies may also cover medical expenses incurred due to injuries that occur within the business’ premises, regardless of who is at fault or whether a lawsuit has been filed.

General liability insurance is not legally required for you to operate a business in the US. However, some clients, stakeholders, and suppliers may make this type of coverage a condition for doing business with you.

Although some businesses face greater liability risks than others, it is always advisable to purchase general liability coverage as it provides financial cushion in the event your business is sued because of an unexpected accident. General liability insurance is a crucial form of protection if your business:

-

- Has a store, office, or premises with heavy foot traffic

-

- Sells products or provides services

-

- Handles or conducts work for or near a client’s property

-

- Uses social media as part of your operations

-

- Creates advertisements or marketing materials for your business

-

- Needs coverage to be considered for work contracts

Each business faces its own share of unique risks and challenges. Because of this, general liability insurance alone is not enough to provide complete coverage. Here are the other types of policies that your business needs to ensure that you are covered for any unexpected incident:

-

- Workers’ compensation insurance: A requirement in almost all states, workers’ compensation insurance pays out the cost of medical care and a portion of lost income of employees who become injured or ill while doing their jobs.

- Commercial auto insurance: All commercial vehicles are required to carry this type of coverage for them to be legally allowed on US roads. It operates under the same principle as personal car insurance, providing coverage for third-party bodily injury and property damage resulting from a collision.

- Health insurance: If your business has more than 50 full-time employees, you are required to take out health insurance for your staff, according to the Affordable Care Act (ACA). But if you have less than 50 employees, you can access ACA’s Small Business Health Options Program (SHOP) as coverage.

- Commercial property insurance: Also referred to as business property or commercial building insurance, this policy is designed to minimize disruption to your business’ day-to-day operations by providing compensation for damages or losses that happen to the property your company operates in. This form of coverage is also often a requirement for commercial leasing arrangements.

- Professional liability insurance: Also known as errors and omissions (E&O) or malpractice insurance, this type of policy protects your business from work-related claims, including discrimination, mismanagement, and harassment. It also covers legal and settlement costs arising from service-related mistakes and oversights.

- Directors’ and officers’ (D&O) insurance: This type of business insurance is designed to protect the directors and senior management of a company against financial losses resulting from business-related lawsuits. It pays out for monetary losses resulting from these legal actions, including defense costs, settlements, and fines.

- Business interruption insurance: Also called BI or business income coverage, this policy is designed to protect your business against financial losses incurred from the disruption of your operations due to a covered peril.

- Cyber insurance: Cyber policies protect your business against financial losses resulting from cyberattacks.

Business insurance plays a vital role in providing your business with financial protection from unexpected events that can otherwise cost you several thousands, if not millions, in income, making it difficult for you to recover. If you want to find out how this form of coverage can help you navigate difficult times, you can check out our comprehensive guide to business insurance in the US.

Given how much general liability insurance costs, do you think it is a worthwhile investment? Is this type of coverage enough to protect your business? Feel free to share your thoughts in the comments section below.

Related Stories

Keep up with the latest news and events

Join our mailing list, it’s free!